.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Tokenization has grown in prevalence as one of the leading security technologies of this decade.

In the payment industry, tokenized payments have taken hold of the industry’s biggest players. Visa announced in June 2024 that they have issued a total of 10 billion payment tokens.

It’s not just in payments, either. Tokenization has widespread use cases across all industries, especially those dealing with the management of sensitive and private data. It even has compelling use cases for functions like identity verification and asset ownership.

Could tokenization be the future of digital security?

To find out, we’re discussing the technology in-depth, including how it works and its various applications, along with a deep dive into its use in payments.

What is Tokenization?

Tokenization is the process of replacing sensitive, confidential data with non-valuable tokens.

A token itself holds no intrinsic value or meaning outside of its intended system and, without proper authorization, cannot be used to access the data it shields.

Compared to encryption, another popular cybersecurity method for protecting data, tokenization does not simply transform data but replaces it entirely, eliminating the need for a cryptographic key to decipher. Instead, the token stands in place of data held securely in a vault.

Tokenization has many applications across many industries. For instance, healthcare organizations can use tokens to protect patient records when transmitting them across healthcare systems. Meanwhile, a payments company can also use tokenization to protect customer payment data during a transaction.

The wide-reaching use cases of tokenization have helped the technology to grow in prevalence quickly, with the global tokenization market expected to reach a value of more than $16 billion by 2032.

Application of tokenization tends to be context-specific, often working best in environments tailored for managing those tokens. The broad security benefits that tokens can offer make it a worthwhile investment consideration for businesses across different sectors, as it can assist both with protecting data and meeting current regulatory requirements for data privacy.

How Does Tokenization Work?

On the most basic level, tokenization works by issuing unique digital tokens that represent real data.

Tokens act as placeholders, with a table of tokens and the corresponding data stored elsewhere in a secure location. Who stores those token tables depends on the type of tokenization (more on that later), but generally, tokens are kept in a controlled environment, such as within a specific payment network.

When the transmission of data takes place (be it of personal records, payment information, or other types of sensitive data), tokens are sent through the digital systems for the entirety of the process. Once the token reaches its final endpoint, only then can it be decrypted by the authorized parties, typically on separate secure vaults or networks intended for the storage of tokens.

To illustrate how tokenization works, imagine the tokenization process like visiting the library.

At the library, you check out a book with your library membership card. The card itself does not list your name, address, or other identifying information, only your member ID. That member ID cannot be used as a valid form of identification anywhere but the library, as it only has meaning within the library system. If you were to lose your library card, it would not provide anyone with personal information about you. When used at the library, however, the membership card authorizes you to check out books.

Now, apply that same logic to tokens. Tokens do not have meaning outside of the systems which they were made for, but within those systems, they make it possible to authorize a variety of different actions.

In real-life use cases of tokenization, there are also additional security measures in place to keep tokens protected from unauthorized access when not in use.

The Different Types of Tokenization

While we can talk generally about tokenization technology and how it works, there are many unique types of tokenization, and each functions slightly different from the rest.

The main types of tokenization used today include:

Network Tokenization

Network tokenization is designed with payments in mind, replacing sensitive card data with a token provided directly by the issuing card network (i.e. Visa, Mastercard, etc.). A network token can be unique to each merchant and is used to substitute a card’s primary account number (PAN).

Businesses dealing with recurring payment and billing models find network tokenization particularly advantageous. It allows these businesses to continue charging recurring bills, such as subscription services, without requiring direct payment interactions with the customer each billing cycle.

The network tokens keep the card payment data refreshed with the latest information and credentials, simplifying data privacy and payment performance for merchants and marketplaces.

PCI Tokenization

Unlike network tokenization, which replaces a PAN with a token across the entire payment ecosystem, PCI tokenization replaces a PAN at a specific endpoint. PCI tokenization is designed to align with PCI DSS standards for payment data privacy and security, a key component of which is storing the payment information and tokens in a PCI-compliant vault.

Merchants and marketplaces can use PCI tokenization solutions to reduce their compliance burden, though compliance can be simplified with network tokenization as well. While network tokenization is managed by the card networks, PCI tokenization is managed by PCI-compliant service providers.

Digital Wallet Tokenization

Digital wallet tokenization uses tokens to represent payment information stored within a digital wallet, such as Apple Pay, Google Pay, or PayPal. Most major digital wallet providers (i.e. Google, Apple, etc.) use a combination of device authentication and tokenization technologies to offer users comprehensive security when transacting with their wallet.

Advanced Forms of Tokenization

In addition to the three types of tokenization discussed above, there are also more advanced versions of the technology. Web3 tokenization, for instance, uses tokens to make financial assets more accessible. This could include tangible financial assets, like art or real estate, as well as intangible assets, such as your intellectual property rights.

Per a 2024 McKinsey article, tokenized financial assets could reach a market cap of $2 trillion by 2030.

AI tokenization is another example of advanced applications of the token technology. This type of tokenization is used by large language models (LLMs) to make training and input data easier to understand, such as splitting text into individual word tokens.

The Benefits of Tokenization

Tokenization is an advantageous technology for multiple industries due to its ability to provide both protection and efficiency. Fraud prevention and cybersecurity measures can sometimes find themselves at odd with operational efficiency, as it takes time to employ proper checks and controls.

With tokenization, security is handled at the storage level, while tokens are safely transmitted for various functions without putting the real data at risk. If the tokens are compromised during transmission, the actual information remains safe and inaccessible to the unauthorized party.

The use of tokens also helps tremendously with compliance, especially in industries like finance and healthcare where data use and privacy regulations remain strict.

Additional benefits of tokenization technology can include:

- Improved customer experiences and heightened customer convenience

- Seamless checkout experiences with high authorization and approval rates

- Reduced legal liability when using sensitive data

- Limited exposure of sensitive data, leading to reduced fraud vulnerabilities

- Simple integration with modern digital systems, including digital and mobile channels

What is Payment Tokenization?

Payment tokenization is the application of tokenization technology within payment environments.

Network, PCI, and digital wallet tokenization are all commonly used for payment scenarios to help bring greater security and trust into digital transactions. Only authorized systems (such as card networks or payment service providers) can map payment tokens back to the original financial data, making it easier to keep customer and business payment information safe.

When tailored to applications within the payments ecosystem, tokenization can pose significant benefits for protecting financial data and improving the overall payment experience. Tokens offer tremendous efficiency and reduce the occurrence of payment failures due to bad or outdated information, and with higher authorization rates comes improved payment performance and greater customer retention.

Payment tokens are only valid in specific contexts, such as when passing from a specific merchant back to a card network for authorization. This approach is particularly suited for the payments industry, where each transaction carries unique security challenges depending on where it takes place geographically and the general risk profile of payments within that region.

When are Payment Tokens Used?

Tokenization can be used for every payment that passes through your system, if you so choose. With token technology, you can add a stricter layer of security to your payment system and reduce the burden of compliance for your business.

Although tokenization can be beneficial for all payment scenarios, it is particularly advantageous in a few key scenarios:

Recurring payments

Payment tokenization simplifies recurring payments by securely replacing sensitive card details with reusable tokens, meaning a merchant need only request that token to initiate the recurring billing cycle.

When a recurring payment is due, such as a monthly subscription, the merchant uses the token to process the transaction without needing to store or repeatedly request sensitive card data. Tokenization supports automatic updates for card details when cards are reissued or expire, ensuring uninterrupted recurring billing without requiring customer intervention to correct their payment information.

Payment tokens eliminate the need to handle raw card data and minimize the risk of breaches, making recurring billing cycles a seamless process for both customers and subscription-based businesses.

Mobile payments

Tokenization can improve mobile payment processing by ensuring card details are never exposed during a transaction, even in more vulnerable digital environments like mobile devices.

When a user adds their card to a digital wallet like Apple Pay or Google Pay, the system generates a device-specific token linked to that card. This token is used for each payment instead of transmitting raw card details, making it easy for customers to pay in a few clicks without having to re-enter their payment information every single time. At the same time, it keeps their information safe through tokenization.

E-commerce

Along with mobile devices, e-commerce storefronts tend to be a hotspot for fraud attempts.

Tokenization adds a necessary additional layer of security to e-commerce environments that keeps both businesses and their customers safe. For merchants, tokenization offers a streamlined method for transacting with customers. For marketplaces, token technology can be a key enabler to simplifying marketplace payments, including payouts to merchants and suppliers.

Using tokenization enables e-commerce businesses to never even deal directly with the payment data itself. Merchants and marketplaces never need to worry about storing or encrypting payment information during a transaction, as all of those functions are handled by whoever manages the payment tokens (such as a card network or payment service provider).

The Security Impact of Payment Tokens Can’t Be Ignored

As we’ve covered, payment tokenization can substantially enhance the security of your payment system.

Payment tokens allow you to mitigate the risks associated with handling sensitive financial data. Replacing card details with a meaningless token makes it easy to initiate payments and send the relevant data to financial entities for authorization and approval without ever putting the data at risk.

Should a breach occur during the transaction, the payment token leaves the hacker without a reward to reap. Without access to the token table that reveals what data corresponds with a specific token, there simply is no valuable information to gain from it. Even a successful breach of your payment system can yield few results if the criminal cannot access your token vault of choice.

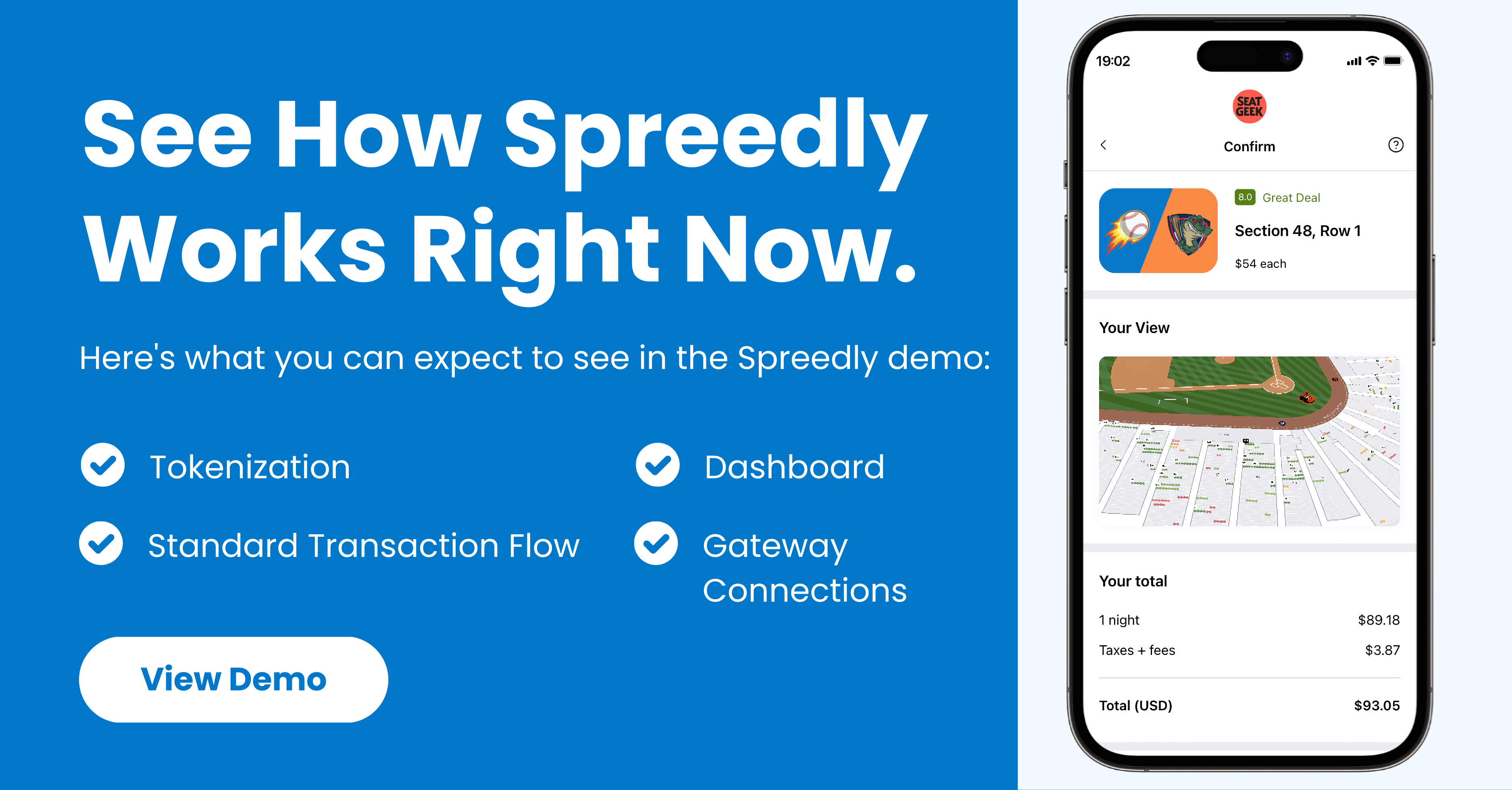

Spreedly’s Advanced Vault Supports Both PCI and Network Tokenization

Spreedly’s open payments platform drives better payment performance.

With our Advanced Vault, you can tokenize and secure your payment data. Spreedly supports all of the token types discussed above, including PCI and network tokens. With PCI tokens, you can transact with virtually any payment service, while network tokens can be added to the vault to help optimize performance. We offer hundreds of connections to help you make Spreedly your control center for all things payments. See how Spreedly works today.

%2520copy.png)

Download the Tokenization eBook

Navigating AI Risk

Building Resilience for Global Scale

Experience how the Spreedly platform can orchestrate and optimize your payments stack.

140+ Payment Integrations

Managed Payment Vault

You'll find everything you need to know about Payments Orchestration in this detailed guide. Find out what you should be looking for, what you'll need to get started, and how to implement changes at every stage.

Navigating AI Risk

Building Resilience for Global Scale

Experience how the Spreedly platform can orchestrate and optimize your payments stack.

140+ Payment Integrations

Managed Payment Vault

.png)