.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

In the Consumer's Eyes: Credit Card vs Debit Card

It is hard to imagine that the introduction of credit cards were piloted by the Bank of Delaware and several years after that other banks started implementing them.

There are literally hundreds of articles, blog posts and multimedia presentations that compare the pros and cons of credit vs debit cards. The conventional wisdom is that using credit cards is a wiser choice. More purchasing power, rewards, credit history building, the possibility of paying later, purchase protection and fraud detection as the advantages of using a credit card vs debit card.

On the other hand, using a debit card can help avoid debt. A third of credit card borrowers pay only the monthly minimum payments. Debit cards cannot damage your credit history because there are no interest and late payment charges.

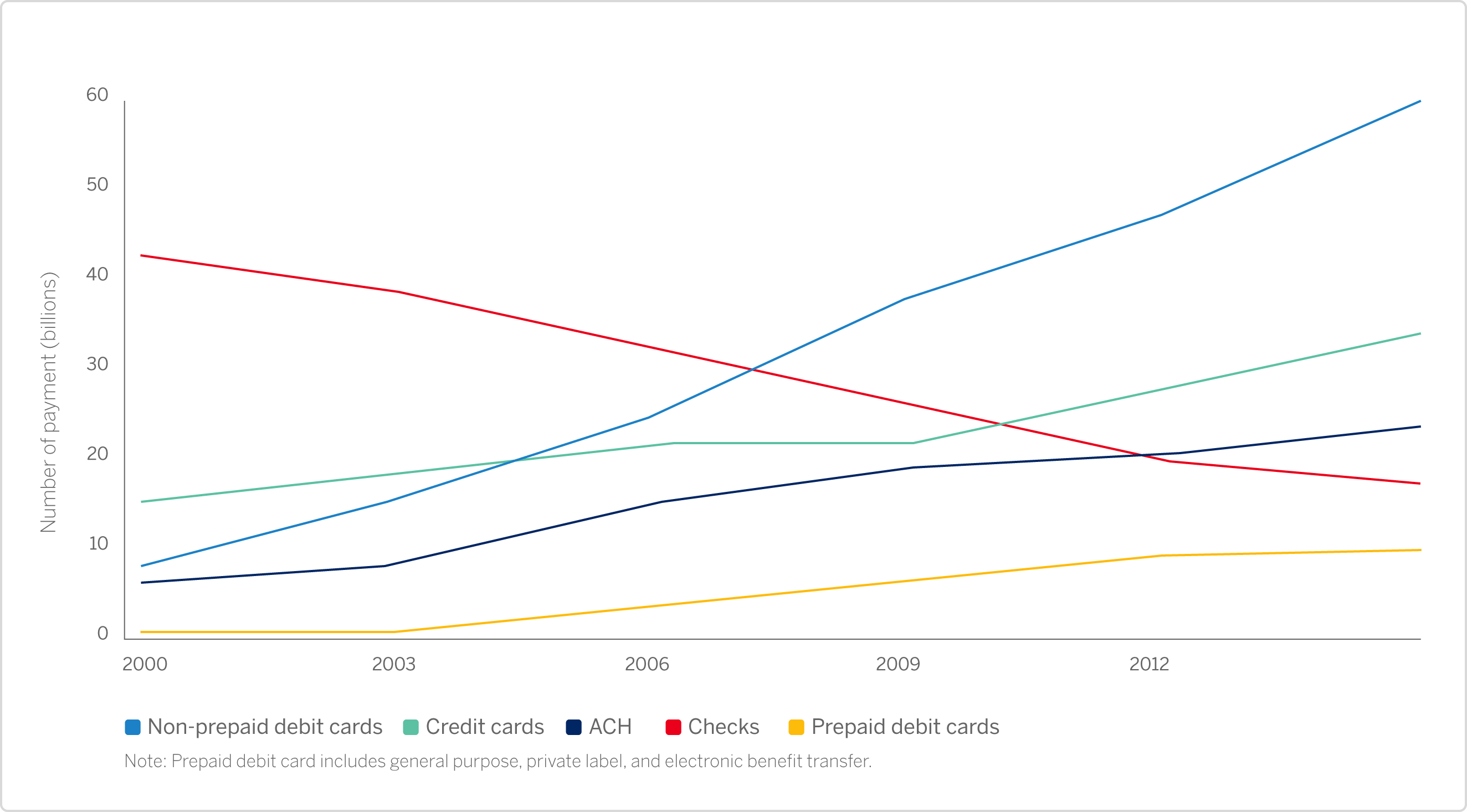

To see how consumers use their credit and debit cards, let's take a look at the most recent federal reserve report. The 2016 Federal Reserve Payment Report shows the growth rate of different payment methods, including ACH (Automated Clearing House) and checks, since 2000. Although the chart shows other payment methods, in this report we will only focus on credit and debit cards.

Processing Fees

While there are many reasons for consumers to use a credit card vs debit card, merchants have one good reason to encourage otherwise. Credit card processing fees. Because debit card transactions travel directly to the customer's bank account they avoid the credit card processing networks. Compared to credit cards, this makes processing a debit card simpler and consequently cheaper.

Generally speaking, PIN-based debit card transactions will end up being cheaper for your business in the long run. When a PIN-based debit card transaction takes place, instead of traveling through the payment networks required to process a transaction as credit, the transaction, along with the customer-entered PIN number, travels directly to the customer's bank account. That account is checked for availability of funds and, if there's enough to cover the requested payment, the account is immediately debited and the funds are scheduled for deposit into your business's bank account within 24-48 hours.

Credit cards distinguish themselves from debits by providing a variety of services that debit cards simply do not offer. However, these services come with higher fees associated with credit cards. When you pay by a debit card, the merchant does not have to need to have the credit card vs debit card option in order to avoid credit card fees.

Of course, one may argue that the increase in the number of customers that credit cards bring in offsets their higher fees. However, we need to account for a more vital parameter: decline rates.

The Cost of Declined Transactions

To account for the true cost of declined orders, one should take into account customer acquisition cost, customer lifetime value, and impact of declined or blocked orders.

estimates that lowering false positive transactions leads to a sales revenue increase of anywhere from 3% to 30%.

Based on lowering or eliminating declined transactions leads to an increase in cash flow, better customer relations, and lower card processing fees.

While fraudulent transactions or lack of funds comprise a big chunk of declines, the problem of false declines by issuing banks is worth further investigation. In particular, we are interested in addressing the following questions. What are the differences in decline rates of credit and debit cards among card brands like Visa and MasterCard, issuing banks, and currencies?

Credit Card vs Debit Card Decline Rates: Overview

Considering the fact that processing a debit transaction is different from a credit transaction, are there significant differences in decline rates between the two?

We used Spreedly data to analyze 8 million payment methods used in more than 22 million transactions in 2016. All payment methods are issued in the United States. And there is an almost equal distribution in the payment methods between credit and debit cards. We compare the performance of a credit card vs debit card by investigating.

Before starting the analysis, we should note that a declined transaction is associated with a handle debits and credit cards.

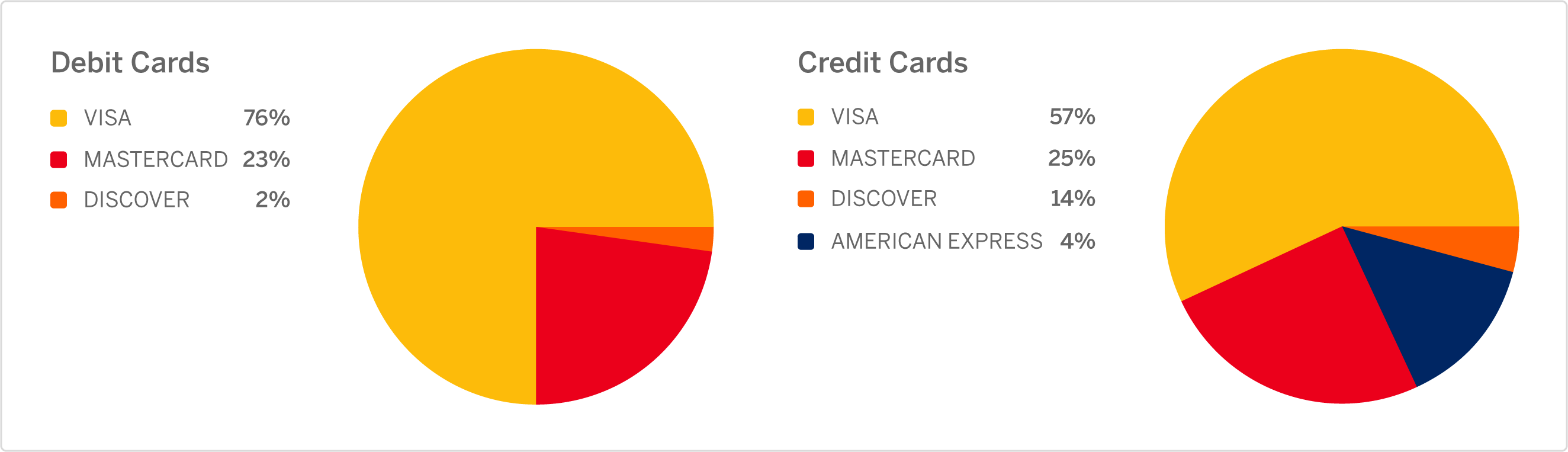

And while 14% of the credit cards belong to American Express (Amex), there are too few Amex debit cards to contribute to the pie chart (left).

Our data shows that 9% of debit and 5% of credit cards in this study have been declined at least once. Considering the equal number of debit and credit cards (around 4 million each) in this study, this difference is noteworthy.

Let's dig deeper and see how card brands declines differ from one another.

1. Card Brands

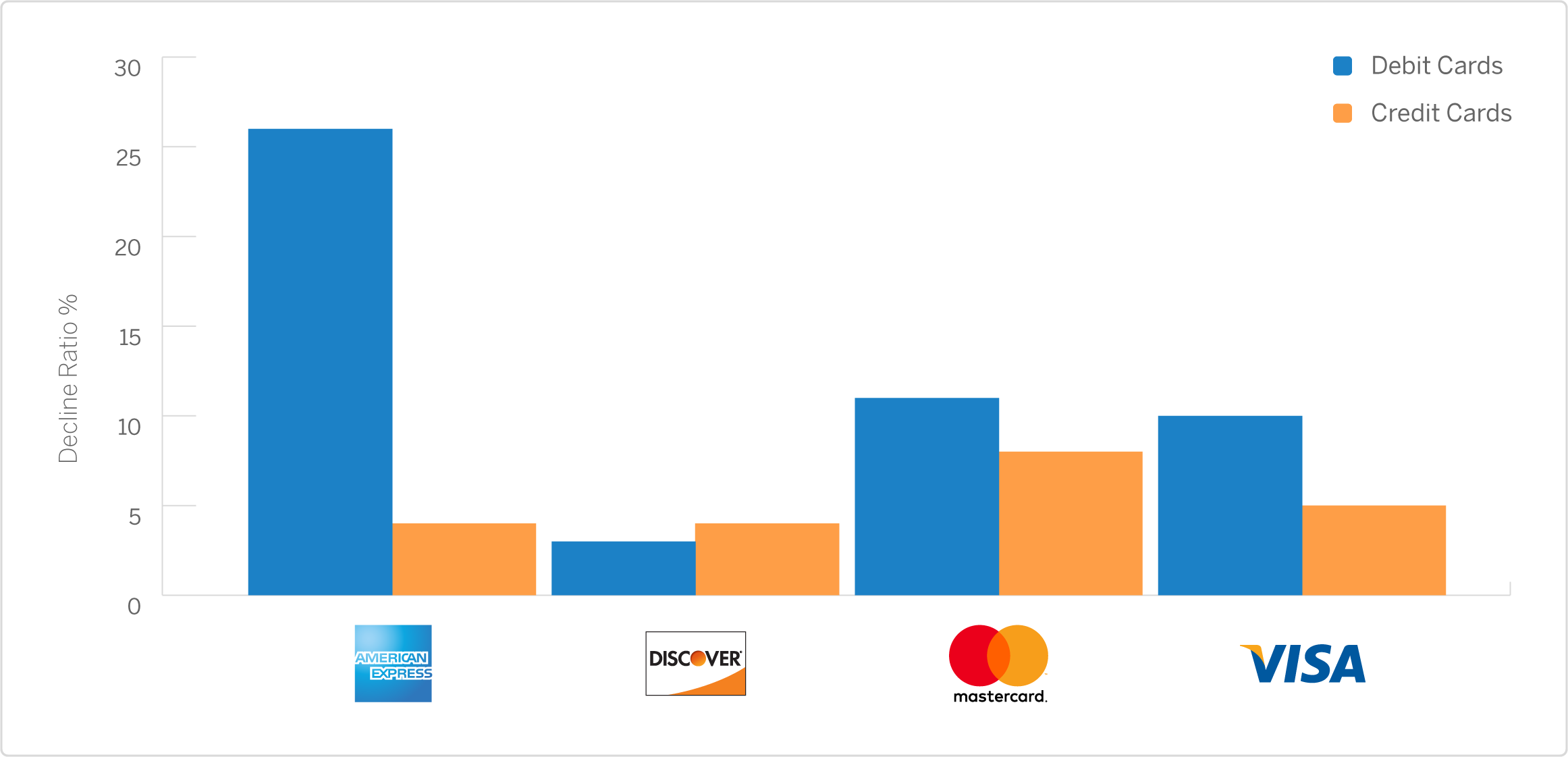

The comparative study of decline rates for card brands provides insights into which brands take more effective measures for processing transactions. Figure 3 shows credit and debit decline ratio (ratio of declined over total transactions) for Amex, Discover, MasterCard, and Visa.

The total number of transactions differ from credit to debit cards, and from one brand to another. In order to make a better judgment, we introduce a ratio of total credit to total debit transactions in each brand. This ratio for all four cards is as follows:

That is, for every 1 debit card transaction on Visa they do 0.69 credit transactions. Also, with respect to the number of transactions, Visa >> MasterCard >> Discover >> Amex. This, in turn, doesn't allow the low declines of Discover to mislead us since they have a much smaller number of transactions processed compared to the other brands.

One also should note that considering the much higher transaction numbers for Visa, it performs better compared to its closest competitor, MasterCard.

2. Issuing Banks

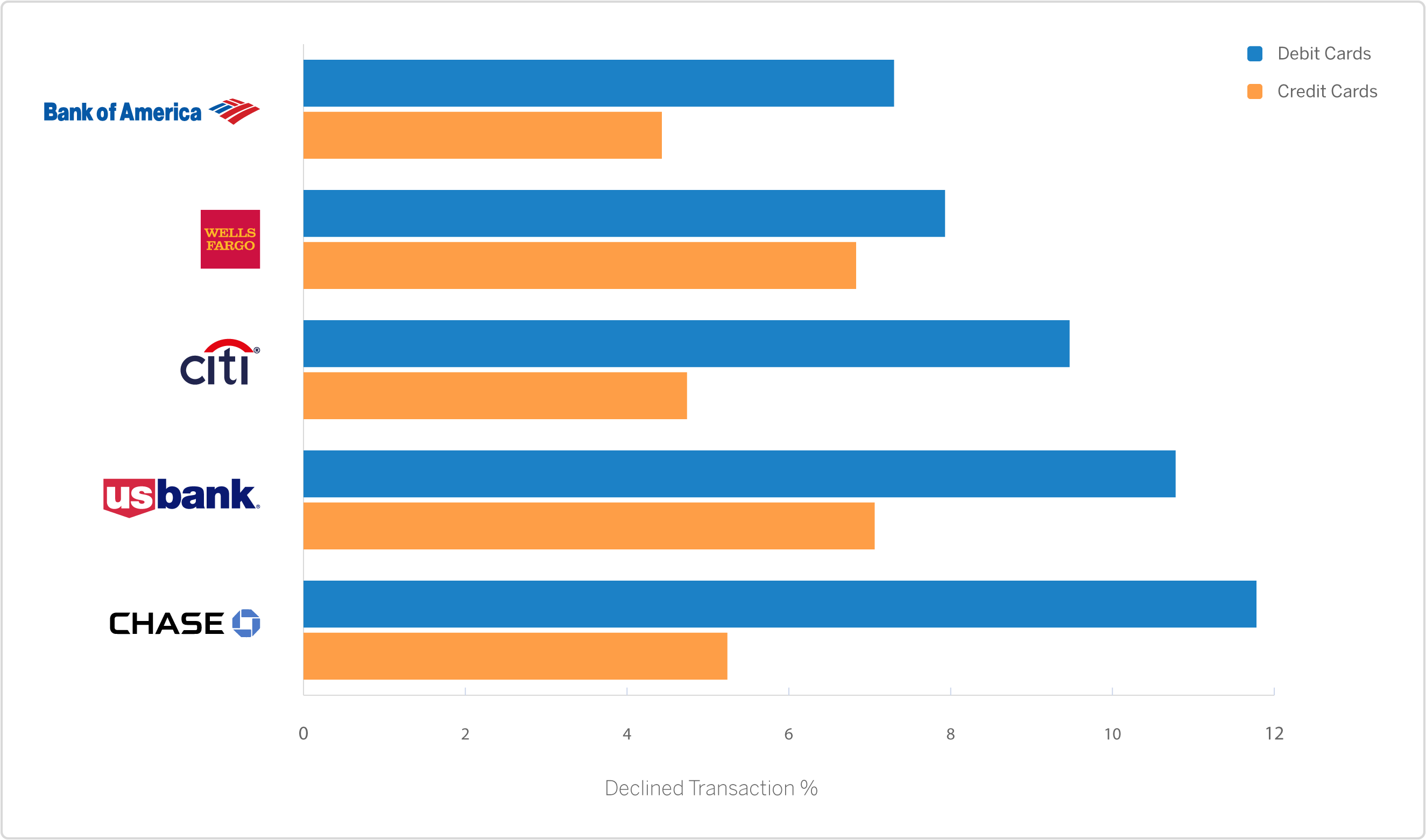

The issuing banks have their own fraud protections in place and play a vital role in approving or declining transactions. In this section, we evaluate the performance of the issuers, disregarding the card brand. We want to observe whether there is a meaningful difference in their credit card vs debit card success rates. The analysis is performed for the issuers with at least 100,000 credit and debit card transactions.

Our analysis shows the bar plot of debit (dark blue) and credit (orange) declines for the top 5 banks, according to the criteria explained above. It is interesting that all the issuers have a better success rate with a credit card vs debit card. The decline rate for credit varies between 4.5% and 7.5%. At the same time, debit declines vary between 7% for Bank of America to 12% for Chase. In fact, the worst credit card decline rates outperform the lowest debit card decline rates.

Bank of America tops both categories with a ~4% and a ~7% debit decline rate. At 1%, Wells Fargo represents the smallest difference between credit and debit decline rates.

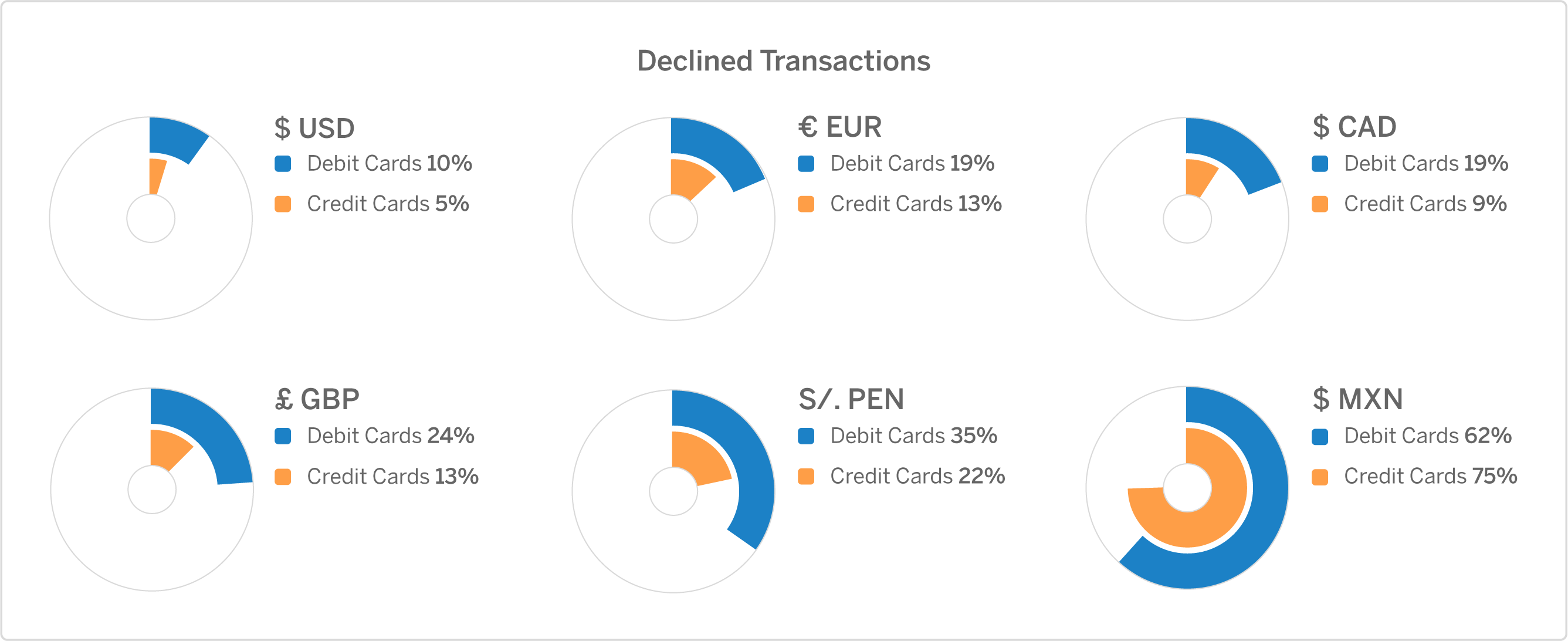

3. Currencies

What about credit card vs debit card performance when traveling abroad or purchasing in currencies other than the United States Dollar (USD)? We can use USD as a measure to compare the decline rate of other currencies.

Euro (EUR) performs better compared to the other currencies in credit card transactions. On the other hand, the Canadian Dollar (CAD) scores better for debit transactions. British Pound (GBP) performs comparatively vs EUR and CAD.

Moving from North America and Europe to Central and Latin America, the decline rate experiences an increase for both credit and debit card transactions. However, in all six currencies below (USD included), credit card decline rates remain lower than debit cards. Purchase protection policies for debit cards are different from those for credit cards. Generally speaking, transactions via credit cards are better protected. With regard to decline rates, for both merchants and customers, our data also shows that using credit cards for a successful foreign transaction is a wise idea.

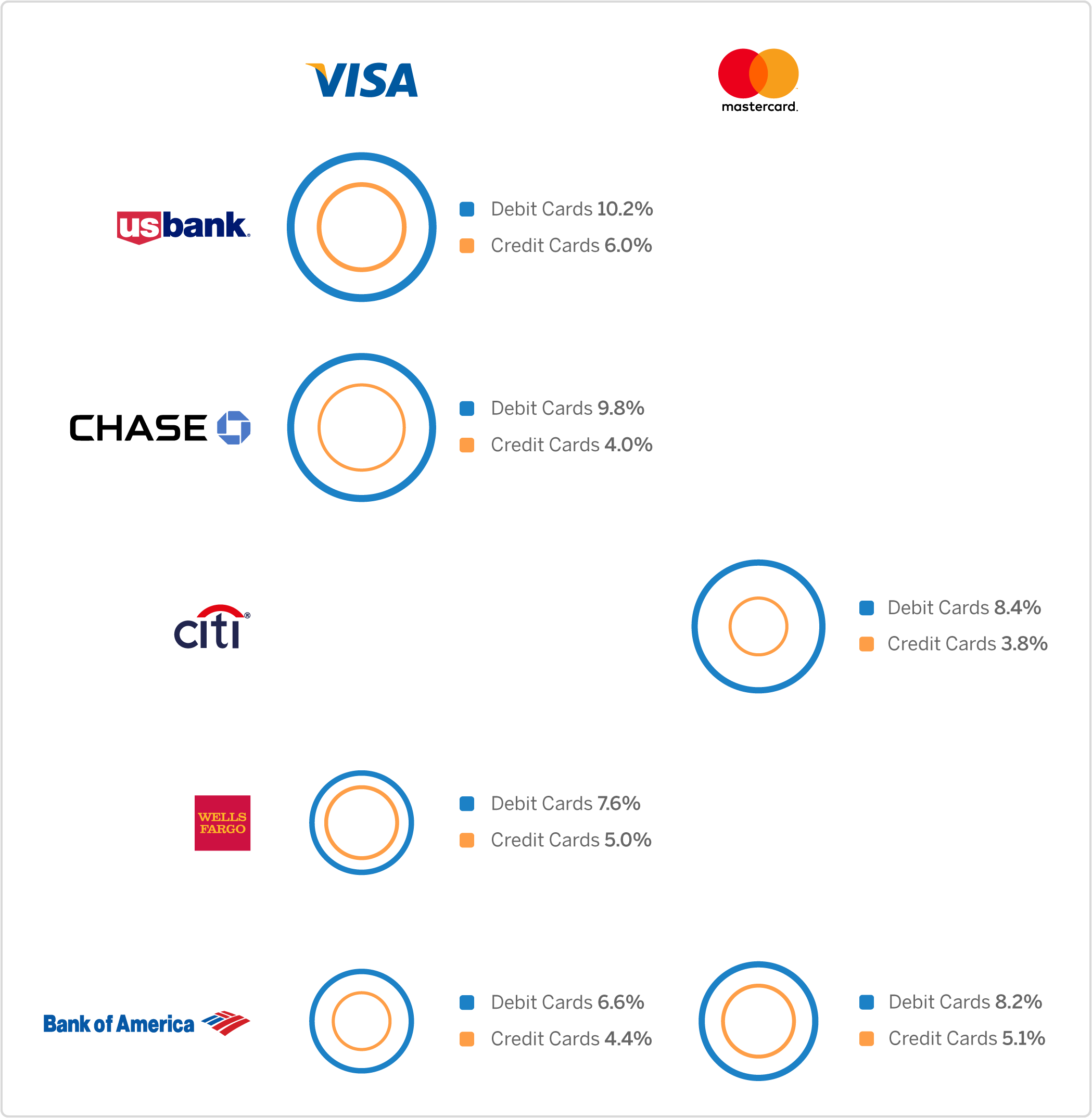

4. Best Card Brand/Issuing Bank Combinations

The issuing banks can work with multiple card brands. At the time of this article, Chase and Bank of America work with both Visa and MasterCard; Wells Fargo and USAA issue Visa and American Express Cards. Hence, after individually investigating the best card brands and banks with the lowest decline rates, it is interesting to study what combination of card brands and issuing banks provide the best (lowest) decline rates.

Here we filter the combinations of card brands/banks for which more than 100,000 transaction records exist. We do this for both credit and debit cards in our database. Due to the small number of Discover and Amex debit transactions, they are left out in this section.

The chart above shows the result of our analysis. Blue and orange circles represent debits and credits, respectively. The numerical percentages are equal to the decline ratio for that card brand/issuing bank.

All the brand/bank combinations in Figure 6 have a better success rate in processing a credit card vs debit card. (The larger circles corresponds to higher decline rates.)

For credit cards, Citi/MasterCard has the best brand/bank combo with only 3.8% decline rate.

For debit cards, Visa/Bank of America ranks first with 6.6% failure.

Among the issuing banks, Bank of America is the only one that handles both Visa and MasterCard exceptionally well.

Conclusion

From the consumer's point-of-view, there are many pros and cons to using a credit card vs debit card. From the merchant's perspective, two important factors should be considered: the cost of processing fees vs decline rates. On the one hand, the higher cost of processing credit cards might motivate merchants to encourage their customers to use other payment methods, such as a debit card. On the other hand, one needs to account for the true cost of a declined transaction: losing a customer. Since this rate is not the same for credit and debit cards the merchant should consider a payment method with the highest upside and lowest downside.

The processing fees for the payment cards are determined by organizations involved in processing the transactions: the cards brands, issuing banks, payment gateways, etc. However, there are very few data-backed studies that investigate the influence of different parameters, like the issuing bank and currency, on decline rates of a credit card vs debit card.

To answer these questions we analyzed about 8 million credit and debit cards and more than 22 million transaction records. All cards in the study were issued in the US. We discussed whether credit cards are worth their processing fees. We also categorized the credit card vs debit card decline rates based on the card's brands, the card's issuing bank, and the transaction currency. In each category, we found that the credit card success rate is much higher than debit cards.

We showed that the issuing banks‚ performance differs in how they handle transactions. We also identified the top banks with the lowest declines. To the best of our knowledge, this is the first time that BIN (bank identification number) database and transactional data are used to the compare the performance of card issuers on such a scale.

Investigating the payments made by US-issued cards in foreign currencies revealed that both credit and debit cards experience an increase in their declines compared to transactions in USD. And except MXN, credit cards are safer and more successful in transacting money in foreign currencies.

We hope that this study sheds light on the crucial topic of decline rates in the payment card industry. And that it helps merchants make more-informed decisions when it comes to choosing the right payment methods.

We capture a tremendous amount of payment performance data here at Spreedly. We work with over 100 payment gateway providers and third party API endpoints worldwide. As such, data that we have access to is qualitatively different than that available to most payment providers. Update: check out part 2 of this series: Cash me if you can: simple steps to lower your credit cards decline rate!

Download the Payments Orchestration eBook Below

Navigating AI Risk

Building Resilience for Global Scale

Experience how the Spreedly platform can orchestrate and optimize your payments stack.

140+ Payment Integrations

Managed Payment Vault

You'll find everything you need to know about Payments Orchestration in this detailed guide. Find out what you should be looking for, what you'll need to get started, and how to implement changes at every stage.

Navigating AI Risk

Building Resilience for Global Scale

Experience how the Spreedly platform can orchestrate and optimize your payments stack.

140+ Payment Integrations

Managed Payment Vault